BYD Saudi Arabia arrived with a plan that feels less like a simple product launch and more like a chess move across an entire industry. The Chinese EV giant is betting that a mixed lineup of fully electric cars and plug-in hybrids — plus deep local partnerships and its Blade Battery — will solve the Kingdom’s practical problems today, while it helps Saudi Arabia chase Vision 2030 targets for electric mobility.

The lead is blunt: many Saudis want electric cars, but the charging network and extreme heat make pure-EV ownership hard right now. BYD’s answer has been pragmatic — sell BEVs where charging is already practical, and push PHEVs where it isn’t. That “bridge” approach is designed to remove the biggest blocker to adoption: range anxiety.

Background: a nation racing to change its car fleet

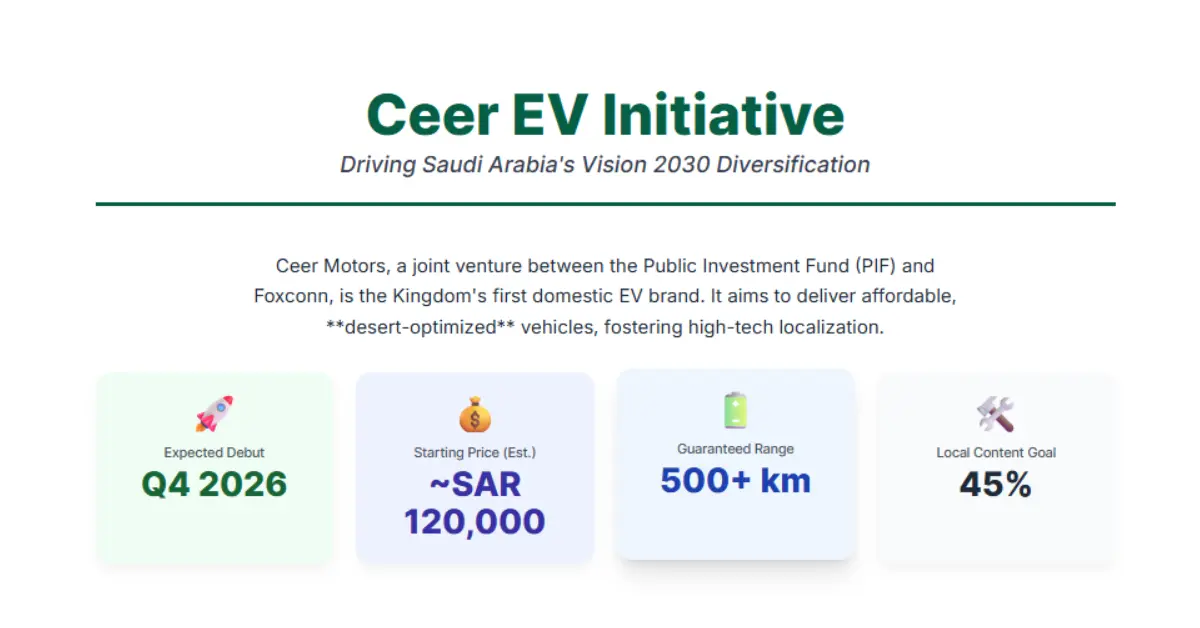

Under Vision 2030, Saudi Arabia wants to diversify away from oil and build a local EV industry. The Public Investment Fund (PIF) is backing big moves — from a local brand (Ceer) to stakes in foreign makers — and state initiatives aim to push EV adoption sharply by the end of the decade. That national focus is why global automakers see the Kingdom as a strategic market, not just another export destination.

Yet the gap between goals and reality is real. Reuters reports only about 101 public charging stations across Saudi Arabia as of 2024, and long routes such as Riyadh–Makkah still lack public chargers, turning long drives into logistical puzzles for BEV drivers. Private and sovereign funds have promised large infrastructure rollouts, but rollout takes time — and car buyers don’t want to wait.

What BYD Saudi Arabia is doing differently

Product mix. BYD’s Saudi line-up includes both BEVs (Han, Sealion 7, Seal, Atto 3) and PHEVs (Song Plus, Qin Plus). The company has said it will bring “more than seven” models to the Kingdom, deliberately balancing all-electric and plug-in hybrid options so customers can choose what fits their daily lives today. The Qin Plus, for example, is offered at an accessible starting price that undercuts many premium rivals, making ownership more realistic for a wider group of buyers.

Local muscle. BYD launched in Saudi operations in 2024 and currently operates showrooms in Riyadh, Jeddah and Dhahran. Jerome Saigot, BYD’s managing director for Saudi Arabia, told Bloomberg the company plans to expand to 10 locations by late 2026 — a physical footprint meant to reassure buyers about service and parts. “Saudi is a complex market. You need to go fast. You need to think big,” Saigot said.

Strategic partnerships. BYD has moved beyond distributors. A Joint Development Agreement with Saudi Aramco signals collaboration on vehicle and energy technologies, while regional partners such as Al-Futtaim provide established distribution and after-sales capabilities. Those relationships show BYD’s intent to be a long-term partner in the Kingdom’s industrial transition, not just a short-term seller.

Technology and climate credibility

Extreme heat is a real, measurable threat to battery life and range. BYD’s Blade Battery — promoted by the company as one of the safest, most heat-tolerant chemistries — is a central part of its message that its cars are “Middle East-proof.” The Blade Battery’s structure and safety testing aim to reduce the risk of thermal runaway and improve durability in demanding operating environments. That technical claim is core to BYD’s pitch in a market where temperatures regularly exceed 40–45°C.

Infrastructure moves, too. BYD has said it will roll out regional ultra-fast chargers — ambitious one-megawatt units that the company says can restore hundreds of kilometers of range in minutes. Whether those stations reach the scale needed to rival national plans (EVIQ’s 5,000-fast-charger-by-2030 aim) is an open question, but BYD’s self-built network helps reduce its reliance on third-party rollout schedules.

iOS 26 Beta Guide: Complete Review for Saudi Arabia Users

A quick snapshot (table) of goals vs reality

| KSA Target / Plan (by 2030) | Current reality (2024–25) |

|---|---|

| 30% EVs in Riyadh | ~1% of national car sales are EVs; early adoption concentrated in luxury segment. |

| 5,000+ fast chargers (EVIQ) | ~1% of national car sales are EVs; early adoption concentrated in the luxury segment. |

| PIF EV manufacturing push ($40–$50bn+) | PIF investments and projects (Lucid, Ceer) actively progressing. |

Expert voices and balanced perspective

Policy papers and consultancies agree: infrastructure, cost and climate adaptation are the three main barriers. PwC’s KSA eMobility Outlook warns that charging coverage and after-sales support must scale alongside vehicle sales, or adoption will stall. At the same time, analysts note tension between state-backed national champions (Lucid, Ceer) and global entrants seeking market share. That creates a competitive but politically significant marketplace where commercial success often depends on local industrial commitments.

“Collaborations like the Aramco deal make BYD more than an automaker — they make it a technology partner,” says a regional energy analyst. But she adds a caveat: “Real industrial integration will require local jobs, supply chains and formal manufacturing commitments — not just agreements on R&D.” Evidence to date shows cooperation, but not yet large-scale local manufacturing from BYD.

Competitive dynamics: Tesla, Lucid, Ceer and the value war

Tesla’s arrival in Riyadh raised the market’s profile by bringing a global brand narrative and charging expectations. BYD’s viewpoint — that Tesla’s marketing educates consumers and helps overall EV interest — is deliberate. BYD’s aim is to capture the mass market with lower prices and a hybrid-first strategy while premium rivals hunt the luxury segment. State-backed Lucid and Ceer complicate the map: they have political backing and ambitions for domestic production, meaning BYD must navigate both market competition and national industrial policy.

BYD’s near-term commercial edge is straightforward: price, a mixed-product portfolio, and localized service. The risk is that aggressive global expansion and price competition can pressure margins and raise political scrutiny. Analysts watching BYD’s global growth note that scale helps, but local manufacturing or deeper domestic investments bolster long-term credibility in a market like Saudi Arabia.

BYD model pricing and consumer value (sample)

| Model | Type | Starting price (SAR) |

|---|---|---|

| Qin Plus | PHEV | SAR 72,900 (starting) BYD Saudi Arabia |

| Atto 3 | BEV | SAR 99,900 (starting) BYD Saudi Arabia |

| Han | BEV | SAR 174,900 (starting) BYD Saudi Arabia |

What this means for Vision 2030

BYD’s playbook — hybrids to cover today, BEVs to win tomorrow, local partners to build trust — is tightly aligned with the Kingdom’s own phased approach: accelerate adoption while building industry and infrastructure. If BYD delivers on showrooms, service, charging and Aramco-level collaboration, it could help push mass adoption beyond luxury early adopters. However, success depends on how fast public charging scales and whether BYD moves deeper into local manufacturing or supply partnerships.

Conclusion

BYD Saudi Arabia is making a low-risk, high-pragmatism bet: solve today’s problems with hybrids and reassurance, then scale the full-electric future as infrastructure catches up. That approach is already earning attention — and sales — but the Kingdom’s journey to 2030 will hinge on chargers, climate-proof tech, and local industrial progress. Readers who follow the EV shift in the Gulf will want to bookmark this story: it’s where policy, industry and daily life meet on the road. Please share if you found this breakdown useful.

Hey, I’m Arafat Hossain! With 7 years of experience, I’m all about reviewing the coolest gadgets, from cutting-edge AI tech to the latest mobiles and laptops. My passion for new technology shines through in my detailed, honest reviews on opaui.com, helping you choose the best gear out there!

1 thought on “BYD Saudi Arabia doubles down — hybrid-first play, Aramco deal, and 10 showrooms planned to beat range anxiety”

Comments are closed.